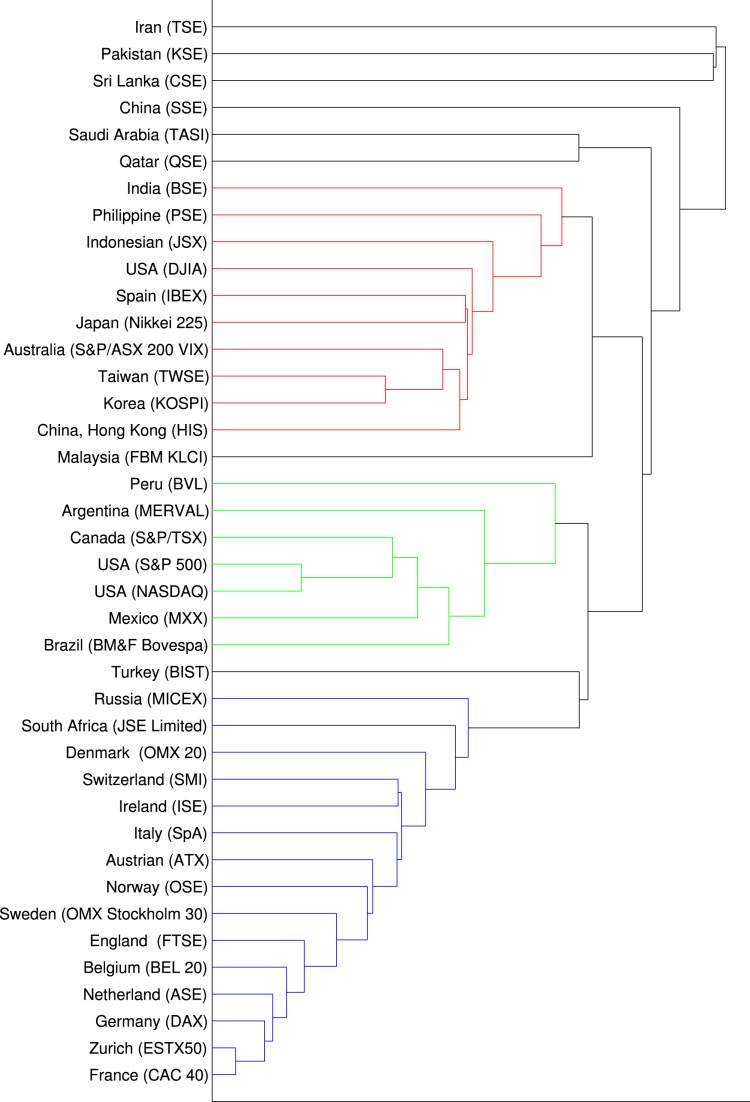

In a recent paper, we studied 40 stock markets from top GDP countries to analyse the correlations and connections between them. As expected, we did observe strong correlations between ups and downs of these markets at the global level. However, when using Random Matrix Theory we detected the sub-communities of this global network, we realised that geography plays an important role.

In this “Brexity” times, the most notable observation is how deep the UK market are embedded in the sub-network of European markets. We often hear that the European partners can be replaced with the US and China. The numbers do not support this!

The paper’s abstract reads:

Forty stock market indices of the world with the highest GDP has been studied. We show each market is a part of a global structure, that we call “world-stock-market network”. Where the correlation between two markets is not independent of the correlation between two other markets. Towards this end, we analyze the cross-correlation matrix of the indices of these forty markets using Random MatrixTheory (RMT). We find the degree of collective behavior among the markets and the share of each market in the world global network. This finding together with the results obtained from the same calculation on four stock markets reinforces the idea of a world financial market. Finally, we draw the dendrogram of the cross-correlation matrix to make communities in this abstract global market visible. The results show that the world financial market comprises three communities each of which includes stock markets with geographical proximity.